According to the Bureau of Justice Statistics, over 6.1 million adults in the United States have a felony conviction. In Georgia, that number hits 730,000 individuals. These people aren’t just numbers—they’re parents, workers, caregivers, and community members.

One major concern among individuals with felony records is: Can I get life insurance with a felony? The short answer? Yes, but it depends. In some states, felonies are broken down into classes (e.g., Class A, B, C), while others use degrees (First-degree, Second-degree, etc.). According to the National Institute of Justice, around 68% of released prisoners are rearrested within 3 years. This risk factor is part of why insurers tread carefully with felony histories.

Does a Felony Automatically Disqualify You From Life Insurance?

No, a felony does not automatically disqualify you from getting life insurance. However, it does complicate things. Most major life insurance companies use your felony conviction as a risk factor, just like smoking, diabetes, or skydiving.

That said, not all felonies are treated equally. And time passed since your conviction plays a big role. If your felony occurred over 10 years ago, and you’ve had a clean record since, many insurance companies may consider your application.

How Do Life Insurance Companies Evaluate Felons?

When reviewing your application, life insurance companies look at:

- Type of felony (violent vs. non-violent)

- How long ago the felony occurred?

- Whether you’re on parole or probation

- Any repeated offenses

- Rehabilitation efforts

- Employment and income stability

- Medical history

- Lifestyle choices (smoking, drug use, etc.)

Insurers might ask:

“Have you been convicted of a felony in the past 10 years?”

“Are you currently incarcerated, on parole, or on probation?”

If you lie on these questions, your policy could be revoked—even after your death.

What are the factors that affect eligibility?

Here’s a list of specific factors that play into your life insurance approval:

| Factor | How It Affects Approval |

| Time since conviction | More time = better odds |

| Severity of crime | Violent = high risk |

| Number of convictions | One = maybe; multiple = less likely |

| Current legal status | On parole = automatic denial in many cases |

| Rehabilitation and employment | Positive history helps |

| Age and health | Good health = better chance |

What types of Life Insurance You Can Get as a Felon?

1. Term Life Insurance

- Offers coverage for a set number of years (10, 20, 30).

- Affordable but harder for felons to get approved.

- Good for family protection or mortgage coverage.

2. Whole Life Insurance

- Lasts your entire life.

- Builds cash value.

- More expensive, but some companies may approve felons with older convictions.

3. Guaranteed Issue Life Insurance

- No medical exam. No questions about criminal history.

- Much lower coverage ($5,000 to $25,000).

- Higher premiums.

- Often used for burial/final expenses.

4. Group Life Insurance Through Employer

- No background check.

- Often available to employees regardless of criminal history.

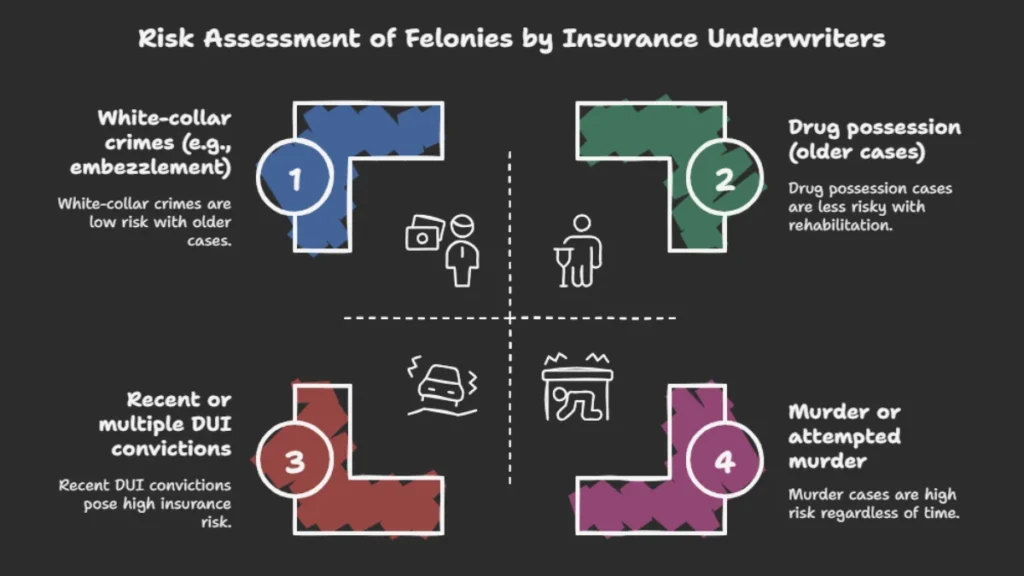

Which Felonies Are Considered High Risk?

Not all crimes are viewed equally by insurance underwriters. Here’s how some are typically ranked:

✅ Low to Moderate Risk (May Be Approved):

- Drug possession (older cases)

- White-collar crimes (e.g., embezzlement)

- Non-violent theft

- Tax fraud

⚠️ High Risk (Often Denied):

- Murder or attempted murder

- Sexual assault

- Child abuse

- Armed robbery

- Recent or multiple DUI convictions

- Drug trafficking or manufacturing

If it’s been more than 10 years and you’ve demonstrated rehabilitation, your chances increase.

Denied Coverage? What to Do Next?

If you’ve been denied:

- Request the Reason in Writing

- You have the right to know why you were rejected.

- Apply With a Different Insurer

- Not all insurers follow the same guidelines.

- Consider Guaranteed Issue Policies

- These policies are expensive but don’t ask about your criminal background.

- Work With a Licensed Insurance Broker

- They know which insurers work with high-risk applicants.

- Wait & Reapply

- Time can be your friend. Reapply after a few years of clean record.

How to Increase Your Chances of Approval?

- Maintain steady employment for at least 2 years

- Stay out of legal trouble

- Complete all parole/probation successfully

- Avoid tobacco, alcohol, and illegal drugs

- Get a letter of recommendation from your employer, probation officer, or clergy

- Be honest in your application

- Work with an independent insurance broker

More Opportunities: Can Felons Travel to Mexico?

Best Life Insurance Companies That Work With Felons (2026)

Here are a few insurers known to be more flexible:

| Insurance Company | Policy Type | Notes |

| Mutual of Omaha | Guaranteed Issue | No health or criminal questions |

| AIG | Final Expense/Whole | Covers many high-risk individuals |

| Gerber Life | Guaranteed Issue | Up to $25,000 coverage |

| Colonial Penn | Guaranteed Life | No questions asked |

| Ethos | Term & Whole Life | More lenient underwriters (case-by-case) |

Avoid companies that only sell high-dollar term life with strict underwriting like New York Life or Prudential unless your record is clean and very old.

Final Thought

Having a felony on your record doesn’t mean life insurance is out of reach—it just means the path might be a little tougher. With honesty, patience, and the right insurer, many felons can still find quality coverage to protect their loved ones. Whether it’s a guaranteed issue policy or full-term life insurance, options exist. Don’t let your past define your future—take action, ask questions, and find a plan that works for you.

FAQs

Can a felon get life insurance while on parole or probation?

Most insurance companies will not approve coverage while you’re under supervision. Wait until you’ve completed parole or probation.

Do insurance companies run criminal background checks?

Yes, they often use public records and third-party data to verify your criminal history.

Can life insurance be denied after it’s issued?

Yes, if the insurer finds out you lied on your application, they can void the policy—even after your death.

Will a pardon or expungement help?

It can, especially if your record is sealed. Some companies won’t consider expunged records during underwriting.